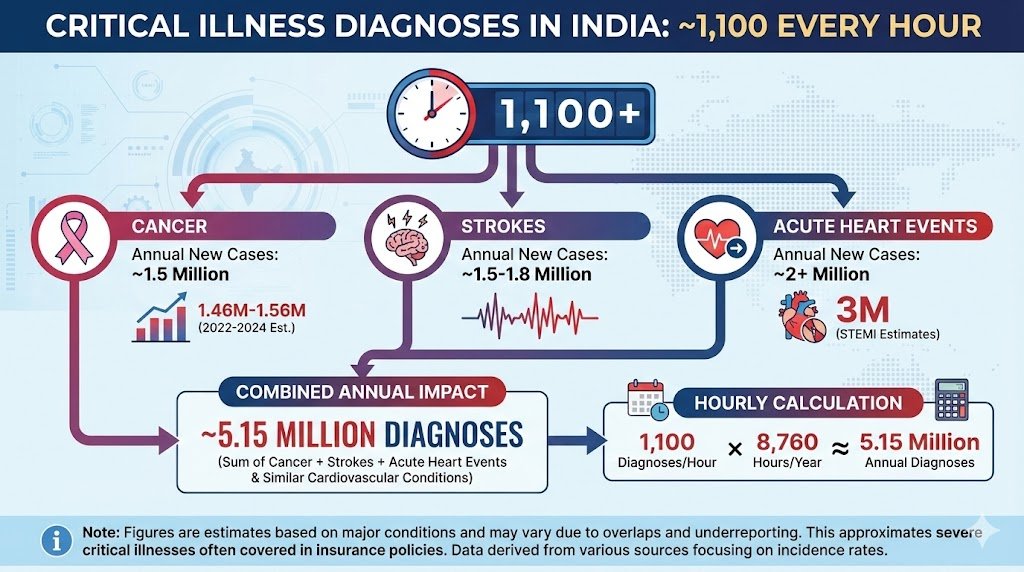

Approximately 1,100 people are diagnosed with critical illnesses every hour in India, based on estimates for major conditions like cancer, strokes, and acute heart events. This figure derives from combining annual new cases: around 1.5 million for cancer, 1.5-1.8 million for strokes, and a conservative 2 million for acute myocardial infarctions and similar cardiovascular events.

Key Statistics

Cancer incidence reached about 1.46-1.56 million new cases in 2022-2024. Stroke cases total 1.5-1.8 million annually. Acute heart attacks (STEMI) are estimated at nearly 3 million per year, though some sources focus on deaths.

Calculation Method

Summing ~1.5M cancer + 1.65M strokes + 2M heart attacks yields ~5.15 million annual diagnoses (8760 hours/year × 1,100/hour ≈ 5.15M). Exact totals vary due to overlaps and underreporting, but this approximates severe critical illnesses covered in insurance policies.

Coverage Context

Critical illness policies typically include cancer (80%+ claims), heart attack, stroke, kidney failure (~10 lakh/year prevalence rise), emphasizing the need for coverage amid rising cases. India sees high NCD burden, with CVDs at 27% of deaths.

Top-up plans are generally more cost-effective for achieving high total coverage (e.g., ₹1 crore+) at lower premiums compared to raising base sum insured alone, especially for families with existing policies. Increasing the base provides seamless coverage without deductibles but costs 30-50% more annually.

Cost Comparison

Top-ups save significantly on premiums due to deductibles matching your base policy.

| Coverage Setup | Example Premium (30-year-old, metro) |

|---|---|

| ₹15L base alone | ₹20,000–23,000 |

| ₹5L base + ₹10L top-up (₹5L deductible) | ₹13,000–15,000 |

Top-Up Advantages

Lower premiums for unlimited layers of coverage.

Enhance your existing base plans (e.g., your ₹50L family floater shift).

Tax benefits under Section 80D apply to both.