Navigating the Health Insurance Maze: Top-Up Plans vs. Increasing Your Base Cover

In today’s rapidly escalating healthcare landscape, having adequate health insurance isn’t just a recommendation – it’s a necessity. But as medical costs soar, many families find themselves pondering a critical question: how do I get enough coverage without breaking the bank? Specifically, should you enhance your existing health insurance by increasing its base sum insured or opt for a more specialized Top-Up (or Super Top-Up) plan?

This isn’t just about picking a random policy; it’s about strategic financial planning and ensuring robust protection when you need it most. As experts in navigating these complex choices, we’re here to break down the dilemma and provide a clear verdict.

The Dilemma: Maximize Coverage – How Do You Do It?

Let’s dissect the two primary approaches to significantly boosting your health cover:

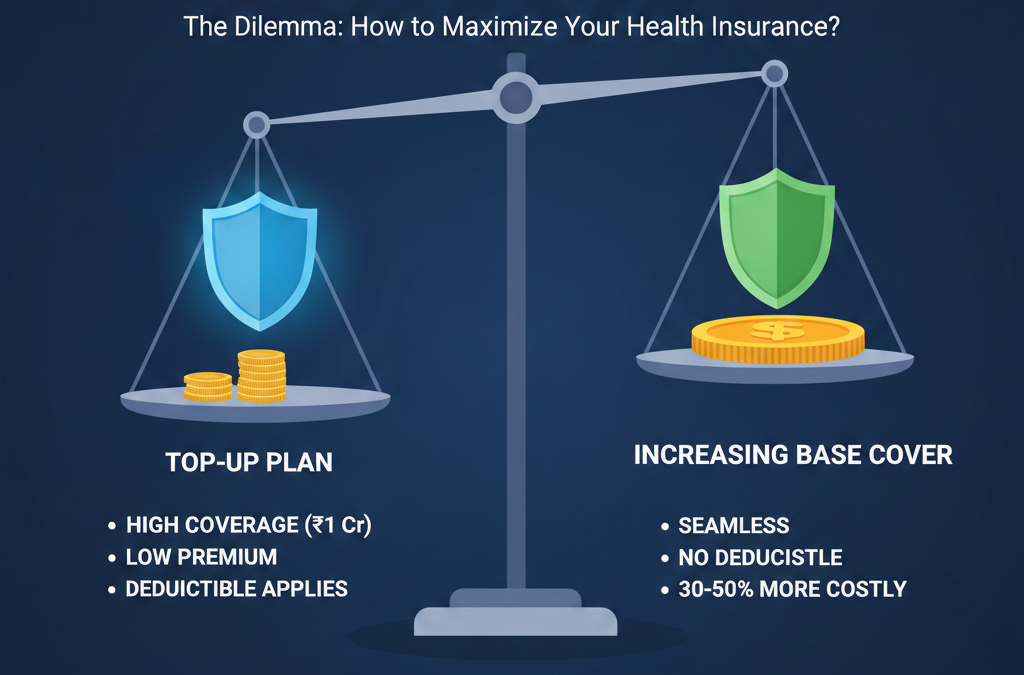

1. Top-Up & Super Top-Up Plans: These plans are designed to kick in after your base policy’s sum insured is exhausted or after a pre-defined ‘deductible’ amount is crossed. Think of them as an umbrella for heavy rain, only opening once the lighter rain gear (your base policy) is overwhelmed.

- Our Verdict: Top-Up plans are an exceptional choice for budget-constrained families and those looking for massive coverage without the massive premiums. They offer an impressive safety net, allowing you to achieve high coverage amounts (e.g., ₹1 Crore) for a surprisingly low cost.

- Key Feature: The deductible. This is the amount you (or your base policy) must pay before the Top-Up plan starts covering expenses.

2. Increasing Your Base Health Insurance Cover: This involves simply raising the sum insured of your primary health insurance policy. If you have a ₹5 Lakh policy, you might increase it to ₹10 Lakhs or ₹15 Lakhs.

- Our Verdict: Increasing your base policy offers a seamless experience with no deductible. Once your policy is active, it covers expenses up to the new, higher sum insured without any initial thresholds. However, this convenience comes at a significant cost, typically 30-50% more than opting for a Top-Up plan to achieve similar high levels of overall coverage.

Our Expert Recommendation: The Smartest Strategy for Enhanced Protection

After years of analyzing policy structures and market trends, our recommendation for most families is clear and strategically sound:

If your existing base health insurance policy is ₹10 Lakhs or more, a Super Top-Up plan is the smartest, most cost-effective way to significantly boost your overall health coverage to ₹50 Lakhs or even ₹1 Crore.

Why a Super Top-Up is the Game Changer:

- Unmatched Coverage for Low Premiums: You gain access to extensive coverage that would be prohibitively expensive if you solely relied on increasing your base policy.

- Leverage Your Existing Base: Your substantial base policy effectively acts as your deductible, ensuring the Super Top-Up only activates for truly catastrophic medical events.

- Tax Benefits Under Section 80D: Like your primary health insurance, premiums paid for Super Top-Up plans are eligible for tax deductions under Section 80D of the Income Tax Act, further enhancing your savings.

By strategically combining a robust base policy with a high-value Super Top-Up plan, you’re not just buying insurance; you’re investing in peace of mind, protecting your family’s health, and optimizing your financial resources against unforeseen medical emergencies.

Ready to explore the best Super Top-Up options tailored for your family’s needs? Contact us for a personalized consultation!